We understand what you are going through because we have been helping people in your situation for over 30 years.

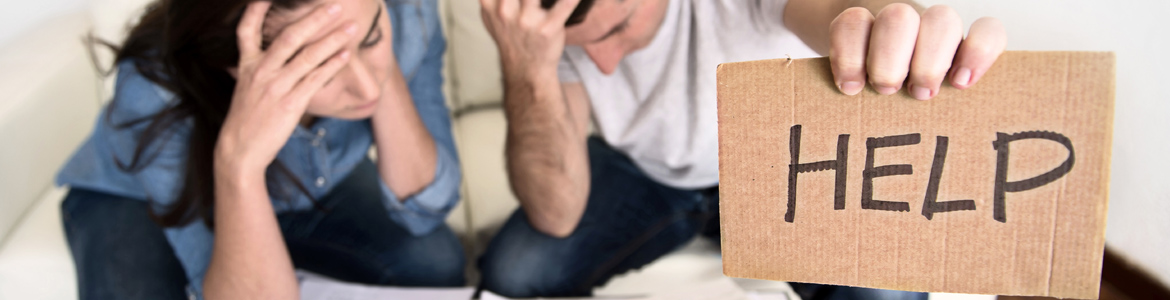

We know how difficult it is to see a lifetime of hard work threatened because of an unexpected situation such as job loss, decrease in income, divorce, death/illness in family or any other hardship that would lead to you losing your home.

We also know how frustrating it is to face a mountain of uncertainty with no clear path to getting back on track. We successfully help hundreds of homeowners every year in similar situations.

When facing foreclosure there is no one better to turn to than our team...

Here is why:

- We have a highly dedicated PROVEN team of experts that have the skills & knowledge necessary to get you started on the road to recovery.

- We have over 30 years of combined experience specializing in foreclosures and short sales. John Bodien was one of the first agents in Michigan to have ever done a short sale. He was doing short sales long before many of us even knew what a short sale was. Most agents were forced into understanding short sales only because of the current economic situation.

- Integral knowledge of the Michigan state laws regarding foreclosures. We are always working hard to make sure we are current on any changes regarding the laws directly related to foreclosures/short sales. A genuine passion to help people in your situation and to fight to make sure you receive the best possible outcome in your situation.

- A vast array of key relationships with necessary resources to help make sure you understand all options available to you. We work directly with a network of bankruptcy attorneys, tax consultants, credit experts, and other valuable resources that are also available to give you FREE consultations to your specific situation to make sure you understand all options that are available to you as well as answer any questions that may arise through out the foreclosure/short sale process. If at any time you don't feel satisfied with our team, you have an unconditional release.. you will owe us nothing, no matter how short or far we are into the process. We do this because we know that if you let us help you, you will not be disappointed with the results.

We have experience processing short sales with Bank of America, Chase, Wells Fargo, Ocwen, CitiMortgage, Select Portfolio Servicing, Caliber Homes Loans, Ditech, Bayview Loan Servicing, PennyMac Loan Services, Mr. Cooper, Carrington Mortgage, Shellpoint Mortgage Servicing, Midland Mortgage, US Bank, PHH Mortgage, Freedom Mortgage, HSBC, Flagstar Bank, LoanCare, Specialized Loan Servicing, Rushmore Loan Management Services, Cenlar, Quicken Loans, and many other lenders.

Understanding the Foreclosure Process

Day 1 to 15

- Typically, payments due on the 1st

Day 16 to 30

- Late charges are assessed after the 15th day past due.

- Loan is in default at 30 days.

- Lender sends notice of delinquency.

- Negotiate a work out plan. Ask "what are my options?"

Day 45 to 60

- Lender attempts phone contact.

- Lender sends out notice that a foreclosure is possible and that borrower has right to contact an attorney and a homeownership counselor to see if borrower is eligible for a loan modification.

- Borrower must contact lender within 14 days from the date the notice is mailed, or Foreclosre proceeds.

Day 90 to 105

- Lender sends "demand" or "breach" letter that the mortgage terms have been violated.

- Once the "demand" letter goes out partial payments are generally not accepted and all delinquent payments and late fees are due.

- Lender hires attorney to initiate foreclosure proceedings.

- Public Notification - Notice of Foreclosure at the local courthouse, details of the debt published in local paper for four consecutive weeks, and a notice is posted on the home.

Day 150 to 155

- Sheriff Sale - House sold at foreclosure sale or auction.

- Title transferred subject to Redemption Rights of the owner.

- The "sheriff's deed" lists the last date the property can be redeemed.

- Redemption period is generally six months, but can be up to 12 months if property is over 3 acres or there is more than 50% equity in the property.

Warning: If you vacate the home the Lender can accelerate or shorten the redemption period.

Redemption Period

- To get the property back you must pay: Mortgage + interest + late fee + court costs + attorney fees.

- EVICTION - At the end of the Redemption Period you will receive an eviction notice.

- LEGAL NOTICE - You will be served with legal notice of action. You can appear in court.

Date is set to actually have the Sheriff move your belongings to the curb.